Dividend Investing UK – Best Dividend Investments 2020

Dividend investing allows you to earn regular income on top of capital growth. For example, by investing in dividend stocks, not only will you make money when the value of shares goes up, but you’ll also receive a dividend payment every three months.

This allows you to enjoy a passive form of income or better – grow your wealth faster by reinvesting your dividends into other assets.

In this guide, we cover the ins and outs of Dividend Investing in the UK. On top of discussing how this area of the financial scene works and covering the best dividend investments right now, we’ll help you get set up with a trading account today.

-

-

What is Dividend Investing?

Put simply, dividend investing is a financial strategy that focuses on assets that yield dividends. This might be a stock that pays dividends or an ETF that distributes your share of profits every quarter. Similarly, bonds are also classed as a dividend investment, as you will receive a coupon payment every 3 or 6 months.

Either way, the overarching concept of this segment of the UK investment scene is that you will be buying assets that payout on a regular basis. At the same time, you still stand the chance to grow your initial investment when the respective stock, ETF, or fund increases in value.

The only exception to this rule are bonds, which can only grow in value if the yield decreases and sell them on the secondary market. Nevertheless, dividend investing is actually one of the most effective ways to create a long-term nest egg. The reason being, by reinvesting your dividend payments as soon as they are received, you will grow your money much faster.

As we cover in much more detail later in this Dividend Investing UK Guide, this is because you will benefit from compound interest. In other words, your reinvested dividends will itself earning interest and thus – this amplifies the rate at which your capital grows. In terms of dividend yields, this will ultimately depend on how much risk is associated with the asset in question.

Dividend Investing Example

Before we continue this guide, it makes sense for us to give you a quick example of how dividend investing actually works.

- You decide to buy 100 GlaxoSmithKline shares

- At the same time, you also buy 1,000 BP shares

- 1 month later, BP announces that it is going to pay a dividend of 2.41p per share

- This means that you will receive a payment of £24.10 – which is paid directly into your brokerage account

- A few days later, GlaxoSmithKline announced that it is going to pay a dividend of 14.61p per share

- As you own 100 shares, you will receive a total payment of £14.61

All being well, the above process will be repeated every three months with all of the dividend stocks that you hold. In fact, the very best dividend-paying companies are known as ‘Aristocats’. This exclusive club of 60-ish stocks has increased the size of their dividend every year for 25 years or more.

Types of Dividend Investing Assets

If you’re interested in taking a dividend-oriented approach to investing, there are plenty of options at your disposal.

This includes the following:

Stocks and Shares

Most investors in the UK will turn to stocks and shares to earn dividends. There are heaps of UK companies that do just this – especially those listed on the FTSE 100. Over in the United States, there hundreds of stocks that pay dividends. In fact, each and every stock listed on the Dow Jones Index is a dividend-payer.

As noted earlier, the vast majority of dividend-paying shares will make a distribution every three months. Initially, the board of directors will meet to discuss [A] whether or not the firm has the financial means to pay a dividend and if so [B] how much should be paid per share. Once the stock goes ex-dividend, the funds will then be forwarded to your chosen stock broker.

The specific amount that you receive is based on the dividend per stock and of course – the number of shares you hold. For example, if the company pays 40p per stock and you hold 100 shares, you will receive an all-in payment of £40. As we cover in more detail later, you should never choose a stock just because it pays dividends.

After all, you might receive an annual dividend yield of 8%, but if the stock has declined in value by 12% – then you have made a financial loss! Nevertheless, this leads us nicely onto a key point about stock dividends – you stand the potential of earning two forms of income.

This is because on top of your quarterly dividend payments you will also be hoping that the stock price of your chosen shares increases. In fact, this is a must for you to be able to grow your money over time. In its most basic form, if you invested £1,000 into BT shares, after year one you made a 4% dividend yield, and the shares increases by 6% – your all-in gains would amount to 10%.

ETFs and Index Funds

While most dividend seekers turn to traditional stocks, we would suggest that you also consider ETFs and index funds. This is because the fund provider will distribute your share of any dividend payments that it receives. For example, let’s suppose that you invested £5,000 into an ETF that tracks the Dow Jones.

In doing so, the ETF provider would personally purchase all 30 stocks that form the index, and thus – you would be entitled to your share of any gains. It goes without saying that each stock will have a different ex-dividend date. For example, while Apple might pay its dividend on the 3rd Friday of March, Walmart might make a payment a week later.

Either way, it wouldn’t make sense for the ETF to send you 30 individual payments every three months. Instead, it’s far more efficient for the provider to collect all 30 payments and then make a single distribution on a fixed date in each quarter.

- So, let’s assume that you invest £2,000 into a Dow Jones Index ETF

- Over the course of three months, an ETF collects dividends at an annualized yield of 6%

- In theory, this means that you’ll get a quarterly dividend at 1.5% (6% / 4) of your invested capital

- As such, you receive a payment of £30 (£2,000 x 1.5%)

- In quarter two, the ETF collects dividends at an annualized yield of 5%

- This means that at 1.25% (5% / 4), you receive a payment of £25 (£2,000 x 1.25%)

However, it is crucial to note that much like stocks and shares – ETFs rise and fall in value. In the case of the aforementioned Dow Jones Index ETF, this will be dictated by how the value of each individual stock performs. In other words, if the 30 constituents of the Dow Jones collectively grow in value, as will your ETF investment.

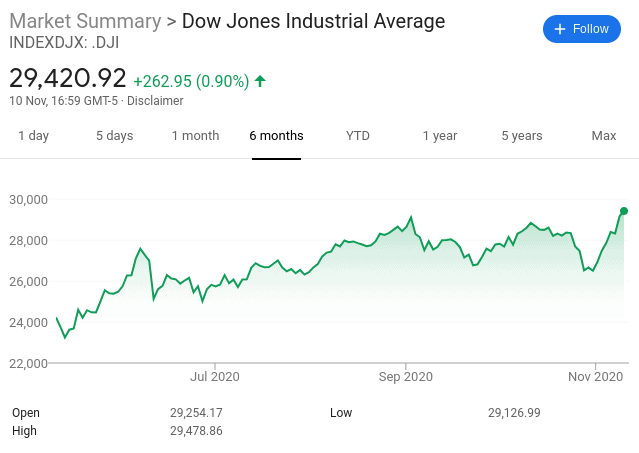

For example, in the 6 months prior to writing this guide, the Dow Jones Index has grown by almost 21%. In simple terms, this means that not only will you have received dividends from the ETF, but your £2,000 investment would now be worth £2,420.

Note: If you are interested in other UK dividend investments like mutual funds or investment trusts – the above process works in exactly the same way. The only difference is that these fund types will look to outperform the market, as opposed to simply tracking it.

Bonds

An additional option that you have at your disposal is that of bonds. While bonds don’t pay dividends per-say, they do attract coupon payments. As such, these are dividend payments in all but name.

The main concept with this UK dividend investment is as follows:

- You purchase 10 bonds at £100 each – taking your total investment to £1,000

- The bonds have a coupon rate of 4% – which is paid bi-annually

- You own 10 bonds so that’s £40 per year – or £20 every six months

- The bonds have a 10-year expiry

- Over the course of the bond term, this means you will receive a total of £400 (£40 annually x 10 years)

- Once the bonds mature, you then receive your initial £1,000 back

Bonds are popular in the UK with those seeking passive investment steams. This is because they require zero input once the investment has been made. On the flip side, it is important to remember that you will only be able to earn dividends and no capital growth. As such, the amount you can earn is predictable, albeit, fixed.

Note: Some bonds can be sold on the secondary market before expiry. The yield attached to the bonds will move up and down depending on market forces. This means that by offloading the bonds early, you could more or less than you originally invested.

REITs

As you likely know, real estate is one of the best ways to earn a regular income. This is because you will receive a rental payment every month. Additionally, your capital can grow when the value of the underlying property appreciates. As such, real estate is a great dividend investment to consider.

Unfortunately, the barrier to entry is huge – as you will either need to buy a house outright or commit to a long-term mortgage. A great alternative to this is to invest in a real estate investment trust (REIT).

In a nutshell, REITs are managed by large institutions. Much like mutual funds and ETFs, the respective provider will collect money from thousands of investors. In turn, it will pool the invested funds together to make real estate purchases. As a so-called shareholder of the REIT, you will be entitled to quarterly dividend payments.

The amount you receive will depend on the real estate portfolio that the provider holds. For example, it might collect rental payments from commercial tenants, shopping malls, hospitals, or retail parks. Either way, this is a great option for combining the fruits of a dividend investment stream and long-term capital growth.

Dividend Investing Yields

In terms of the yield on dividend investments, there really is no one-size-fits-all answer to this. After all, it ultimately depends on the specific asset that you have decided to invest in.

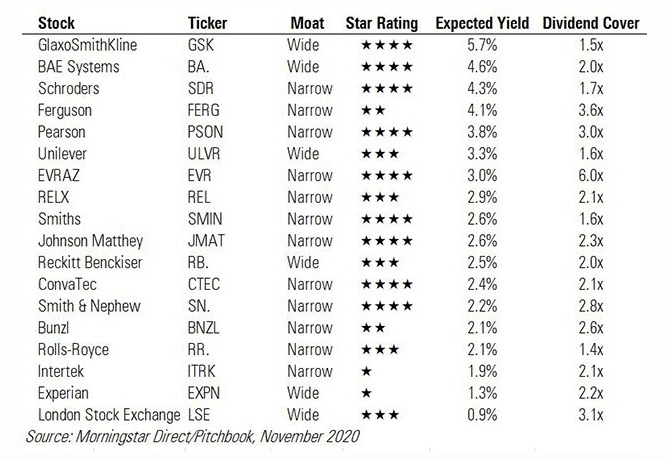

For example, MorningStar notes that the average FTSE 100 dividend yield as of November 2020 is currently 4.7%. This means a return of £470 for every £10,000 that you invest. There are, of course, companies that pay more than this, as well as less.

Companies listed on the Dow Jones, however, pay significantly less at average 2%-2.5%. But, this is because the 30 constituents of the Dow are strong, stable, and highly established companies. As such, although this typically results in a smaller dividend yield, the underlying risks are also low.

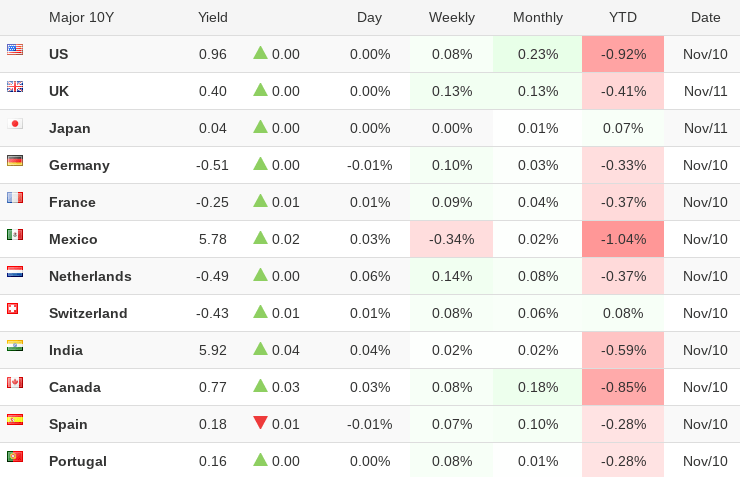

If it’s bonds that you are interested in, the dividend yield (coupon payment) is based solely on risk. That is to say, the higher the risk of default, the more you will receive in interest. For example, 10-year bonds issued by the government of the US, UK, and Japan will yield just 0.40%, 0.96%, and 0.04% – respectively.

Why? Because the chances of these bonds defaulting are virtually zero. At the other end of the spectrum, 10-year bonds issued by Brazil and India will yield 7.24% and 5.92% – respectively.

Benefits of Dividend Investing

Like all investment streams, you need to consider both the benefits and potential drawbacks of the asset in question. As such, we are now going to discuss the pros of making dividend investments in the UK.

Regular Income

The obvious starting point is that you can earn income on your dividend investments without needing to sell or cash out the asset. For example, if you hold £10,000 worth of Apple shares and the stocks annually yield 2% in dividends, you will receive £200. But, you don’t need to sell your Apple shares to get the cash – meaning you can still enjoy long-term capital growth on this tech giant.

Predictable Income

A lot of dividend investments offer a consistent, predictable flow of income. This is especially great for those of you that are put off by wider market volatility. For example, we know that Dividend Aristocats have been increasing the size of their dividend payment for at least 25 years. Some firms – such as US conglomerate 3M, has increased the size of its dividend for over 60 years!

Defense From Falling Stock Prices

Stock prices can both rise and fall – that’s just the nature of the investment game. But, by making stock dividend investments, you can mitigate some of the risks associated with the latter.

For example, let’s suppose that the value of your stock investment is down 8% for the year. But, based on your initial investment, you also received a 3% dividend yield. In turn, while not ideal you are 5% down for the year as opposed to 8%.

Dividend Reinvestment

We cover this particular dividend investment strategy in greater detail shortly. Nevertheless, the main concept here is that dividend investments allow you to engage in a long-term reinvestment plan.

This means that as soon as you receive a payment in your chosen share dealing account, you can use the funds to make new dividend investments.

In turn, these new investments will themselves attract dividends. Over the course of time, this means that you are constantly accumulating more assets and thus – you will grow your wealth at a much faster rate.

Risks of Dividend Investing

As per the above, there are many benefits to making UK dividend investments. However, there are several risks that you also need to consider.

This includes the following:

You Still Need to Pick Winning Investments

Make no mistake about it – learning how to pick stocks and shares can be super difficult. In fact, it can take many years to truly master.

The key point here is that by injecting your hard-earned money into dividend investments, you still need the asset in question to perform well. If it doesn’t, you will end up losing money. This is even the case with bonds, not least because there is always the risk of the issuer defaulting on a repayment.

It is Easy to be Blinded by Running Dividend Yields

When financial commentators discussing dividend yields, they often base this on the ‘running’ rate at the time of writing. This simply means that they tally-up the total dividend payment made by the company over the previous 12 months and then dividend this by the current stock price.

For example:

- Stock ABC paid a total of £10 in dividends over the past year

- The company has a current stock price of £100 per share

- This means that the dividend yield is 10%

On the one hand, a running dividend yield of 10% is super-attractive. However, this only tells half the story. That is to say, the likelihood of having such a higher running yield is that the stock in question has likely been performing badly in recent months.

In other words, it’s all good and well buying a stock because it has a high running yield, but you need to look at the bigger picture. After all, further stock price losses could be in the making.

Growth Stocks Might Make You More Money

By opting for dividend-paying stocks, you stand the chance of making money on two fronts. As we have covered throughout this guide, this includes an increased stock price and of course – the quarterly dividend payments themselves. However, if you are looking to maximize your returns, you might actually be better to focus on growth stocks.

For example, the growth stocks listed below have increased by the following percentage rate in 2020 – as of mid-November:

Bearing in mind that we are still in the midst of a global pandemic, the above returns are nothing short of extraordinary. But, the key point here is none of the stocks listed above have paid a single penny in dividends since they went public.

In fact, this will likely remain the case for many years to come. As such, while you might not receive any income with growth stocks, the long-term upside potential is significantly larger.

Dividend Investing vs Value Investing

There are many types of investments that you can add to your portfolio. For example, on top of dividend investments, you also have ‘value’ investments. For those unaware, value investments are those that are perceived to have a current stock price that is lower than their perceived intrinsic value. The term ‘perceived’ here is crucial, as whether or not a stock is unvalued is subjective.

Nevertheless, a stock (or any asset for that matter) might be classed as a value investment for the following reasons:

- The stock has lost value because of its most recent earnings report – which fell short of market expectations

- The wider markets are down and thus, the stock price of the company has been dragged down (e.g. the COV-19 pandemic)

- The company recently had some bad news published about it – think Boohoo and its scandal on poor working conditions

- Institutional investors haven’t yet realized the true potential of the stock

Crucially, value investing is more concerned about buying stocks and other assets at a discount. This in itself can be a hugely effective investing strategy to take.

On the other hand, dividend investments are purely focused on assets that generate regular income. With that said, investors will still want to concentrate on dividend investments that can also grow in value. For example, this might be an increased stock price over the course of time.

Ultimately, there is no reason why you can’t add both dividend investments and value investments to your wider portfolio!

Dividend Investing Strategies

If you are looking to hone in on a portfolio of dividend investments, you must first ensure that you have some sort of strategy in place. After all, there is never any guarantee that your investment decisions will turn a profit, so having a clear plan of action is crucial.

With this in mind, below we have listed three tips that can help you deploy an effective dividend investing strategy.

Tip 1: Always Reinvest Your Dividends

First and foremost, we can’t stress enough how important it is to reinvest your dividends at the first possible opportunity. This is because you will benefit from the long-term effects of compound interest. As we briefly noted earlier, this means that your dividends will be used to purchase new assets.

In turn, your newly acquired investments will hopefully generate financial gains too. By repeating this process over and over again, your wealth can grow at a much faster rate. In the world of finance, this is known as a Dividend Reinvestment Plan (DRIP).

In order to demonstrate this with a real-world example, let’s look at two scenarios. Firstly, we’ll look at what happens when an investor withdraws their dividend payments out of the broker as soon as the funds arrive. We’ll then compare the same variables but with somebody that reinvestments their dividends each and every time.

Example 1: Withdrawing Dividends

- You invest £10,000 into the stock markets

- To keep things simple, we’ll say that you receive 5% in dividends each and every year

- This means that you receive £500 annually on your £10,000 investment

- 30 years later, you still have £10,000 invested in the stock markets

- You have, however, received 30 years worth of dividends at £500 annually – totaling £15 in payments

Of course, your £10,000 invested would likely be worth considerably more when you factor in the growth of stock market prices over 30 years. However, the key point is that you have made any additional investments during this time. As such, any growth experienced on your shares is based purely on the original £10,000 that you invested.

Example 2: Dividend Reinvestment Plan

- Sticking with the same example as above, you originally invested £10,000 into the stock markets and you also receive 5% in dividend payments every year

- At the end of year one, you have reinvested the £500 that you received in dividends back into the stock markets

- As such, you now have £10,500 invested

- At the end of year two, your 5% dividend yield now amounts to £525. Already, this amounts to £25 more than the previous year

- Again, you reinvest this back into the stock markets – taking your total investment to £11,025

- At the end of year three, your 5% dividend yield now amounts to £551.25. This is £51.25 more than you received in year one.

- Once again, you reinvest the dividends, so your total stock market holding is now £11.576.25

So, after just three years, you have turned your £10,000 stock investment into £11.576.25. And of course – this does not factor in the growth of the stock markets itself. Although this might not sound like a lot of money right now, it is important that we calculate the end result after 30 years – sticking with the same dividend reinvestment plan.

All in all, if you kept reinvesting your 5% dividends back into the stock markets, after 30 years your original £10,000 investment would be worth £44,402. If you also considered adding an additional £200 into your portfolio at the end of each month – this figure would grow to a whopping £211,596!

In turn, by earning 5% per year on £211,596 – you would receive dividends of £10,579 each and every year!

Tip 2: Diversification Will Help Mitigate Your Risks

Financial analysts love to talk about diversification – and for good reason. This simply means that you will be making dividend investments into a variety of assets, markets, and economies, In doing so, you are vastly reducing the risk of being hit by a bad egg.

That is to say, if one of your investments performs badly or worse – goes bankrupt, you won’t feel the impact of this as much if you are diversified into other assets. For example, you might have 50% of your dividend investment portfolio in high-grade stocks, 30% in government bonds, and 20% in REITs.

Within each of these asset categories, you would then need to diversify further. For example, your stock holding might contain dividend-paying companies from the UK, US, and Australia. Additionally, these will come from a variety of sectors – such as retail, banking, consumer goods, and tobacco.

In the case of REITs, most are represented by ETFs. This means that each ETH will have dozens of stocks and index funds that are linked specifically to real estate. You could then make sure that your portfolio contains a good blend of REITs – for example from various housing markets and sectors (commercial, retail, healthcare, etc.).

We should make it clear that creating a diversification plan when making dividend investments can be costly. This is because most online brokers in the UK charge a flat fee every time you invest.

Tip 3: Leave Dividend Investment Decisions to the Experts

As we covered earlier, the process of selecting dividend investments can be extremely challenging. After all, you need to have a firm understanding of how to perform fundamental research and analysis. If you’re a complete newbie, it might be best that you take a step back.

Sure, your chosen asset might seem like a sure-fire bet, but in reality, how will you truly know if you don’t understand financial data? With this in mind, you might want to avoid selecting individual stocks yourself and instead opt for an ETF that focuses exclusively on dividend investments.

- For example – and as we noted earlier, an ETF tracking the Dow Jones Index will allow you to buy 30 different strong and stable dividend-paying stocks.

- ETFs aren’t just reserved for stock market indexes, though.

- On the contrary, there are hundreds of potential ETFs to choose from that buy and sell dividend-yielding assets.

Best Dividend Investments

So now that you the ins and outs of how this particular arena of the financial scene works, we are now going to discuss the best dividend investments available in the UK right now. As always, you should perform your own research to ensure the financial asset in question meets your personal investing goals and attitude to risk.

1. SPDR Dow 30 ETF – Best Dividend Investment for Beginners

We have talked extensively about the Dow Jones Index in this guide. Put simply, this could be the best dividend investment to consider if you are based in the UK and are a complete stock market novice. To clarify, the Dow Jones is a stock market index that tracks 30 large and established companies based in the US.

This includes:

UnitedHealth Group Incorporated 7.90% Home Depot Inc. 6.09% Salesforce.com inc. 5.85% Amgen Inc. 5.30% Microsoft Corporation 4.93% Goldman Sachs Group Inc. 4.85% McDonald’s Corporation 4.81% Visa Inc. Class A 4.80% Honeywell International Inc. 4.45% Boeing Company 4.05% As you can see from the above, the SPDR Dow 30 ETF is weighted. For example, while 4.93% of the portfolio is held in Microsoft shares, 4.05% is held in Boeing. What you will also notice is that the above companies come from a wide range of industries. For example, you have Mcdonald’s from food and beverage and Visa from financial services.

Most importantly, Dow Jones stocks largely have a long-standing and consistent track record of paying dividends. By investing in the SPDR Dow 30 ETF, you will receive your share of dividends every three months. In addition to this, the ETF is listed on the New York Stock Exchange.

Not only does this mean that you can enter and exit your position at any given time during standard market hours, but you will benefit from an increased stock price if and when the Dow Jones performs well. As such, you can combine the fruits of capital gains and regular income with this top-rated dividend investment.

2. iShares Core High Dividend ETF – Best ETF Dividend Investment

As the name suggests, this ETF is focused solely on stocks that have a consistent record of paying high dividends. In total the ETF – which is backed by popular provider iShares, has a portfolio that contains 75 dividend-paying companies.

This includes:

EXXON MOBIL CORP 8.88% AT&T INC 8.86% JOHNSON & JOHNSON 6.44% VERIZON COMMUNICATIONS INC 6.29% CHEVRON CORP 5.93% PFIZER INC 5.67% COCA-COLA 4.12% MERCK & CO INC 3.62% CISCO SYSTEMS INC 3.61% PEPSICO INC 3.55% Once again, the ETF is weighted – so while 8.88% of your portfolio will be held in Exxon Mobile shares, 3.55% will sit with PepsiCo. You will also notice that much like the SPDR Down Jones ETF that we discussed above, your portfolio will be well diversified.

Not only in terms of the number of stocks but the respective industries. For example, you’ve got leading telecommunications companies AT&T and Pfizer from the pharmaceutical scene. What we really like about this dividend investment is that iShares will ensure that your portfolio is automatically rebalanced.

This means that it isn’t afraid to delist an underperforming constituent and replace it with a new stock. If and when it does, your portfolio will be reflected accordingly.

3. iShares Core U.S. REIT ETF – Best Dividend Investment for Real Estate

As we noted earlier, you don’t need hundreds of thousands of pounds to invest in real estate – nor do you need to sign up for a 30+ year mortgage.

As the name implies, this REIT focuses exclusively on US real estate. In total, the ETF basket consists of 150 different instruments. This ensures that you are well-diversified across the entire US housing market.

This includes:

- PROLOGIS REIT INC

- EQUINIX REIT INC

- DIGITAL REALTY TRUST REIT INC

- PUBLIC STORAGE REIT

- WELLTOWER INC

- SIMON PROPERTY GROUP REIT INC

- AVALONBAY COMMUNITIES REIT INC

- EQUITY RESIDENTIAL REIT

Once again, this dividend investment ETF is weighted, with more capital allocated to those that have a greater influence on the wider US real estate scene. In terms of making money, this comes in two forms. Firstly, the ETF provider will distribute a payment every three months.

This will contain your share of any rental payments the provider collected during the quarter. Secondly, you also stand to make money through appreciation. This is achieved through a ‘back-door’ approach, so-to-speak. By this, we mean that you will not directly own any of the real estate, as you are indirectly invested in over 150+ REITs.

But, each individual REIT will increase in value as the properties they own appricate. In turn, this will have a positive influence on the stock price of the iShares Core U.S. REIT ETF. Your investment is listed on the New York Stock Exchange, so even though you are gaining exposure to an illiquid asset like real estate, you can cash out whenever you like.

5. Johnson & Johnson – Best Stock Dividend Investment

While each of the aforementioned investment ideas center on a diversified basket of assets, this particular pick focuses on just one stock – Johnson & Johnson. The reason we have selected this heavyweight US company is that it has a solid track-record that spans over 130 years.

The firm – which is involved in some of the biggest brands found in the pharmaceutical, medical, and consumer good spaces, is valued at over $400 billion on the New York Stock Exchange. Not only is Johnson & Johnson is a Dividend Aristocrat – but it also meets the criteria of a Dividend “King”.

This means that it has increased the size of its dividend payment every year for at least 50 years. In the case of Johnson & Johnson, this now stands at 57 years. As a result, this dividend investment is one of the strongest and most predictable stocks globally.

We would be doing Johnson & Johnson a disservice if we only focused on its superb dividend history. This is because the stock has also rewarded investors over the course of time with its ever-growing share price. For example, you would have only paid about $1.75 (adjusted for stock splits) back in 1980.

In today’s market, the very same Johnson & Johnson share will cost you $148. This means that in 40 years, your investment would have grown by over 8,300%. This means a £5,000 investment back then would be worth more than £42,000 today. Crucially, not only does this exclude dividend yields, but also the added impact of a Dividend Reinvestment Plan.

Best Platforms for Dividend Investing

Once you have decided which dividend investments you wish to make, you then need to find a top-rated broker. There are plenty of trading platforms available to UK investors – some better than others. For example, while some brokers allow you to make dividend investments without paying any commission, others charge a high flat fee.

To help you separate the wheat from the chaff, below we list the three best brokers for dividend investing in the UK.

1. Fineco Bank – Advanced Platform with Portfolio Management

Fineco Bank is relatively unheard of in the UK investment scene as the provider is actually an Italy-based bank. However, it is clearly looking to take the UK investment and trading arena by the horns as it now offers some of the lowest fees in the space.

Fineco Bank is relatively unheard of in the UK investment scene as the provider is actually an Italy-based bank. However, it is clearly looking to take the UK investment and trading arena by the horns as it now offers some of the lowest fees in the space. While not commission-free, you will pay just £2.95 per trade when buying ETFs and stocks. This means that you will have access to heaps of dividend investments at super low fees. In addition to DIY investing, Fineco Bank offers a range of automated, pre-packed portfolios. This will be built based on your financial goals.

As such, by specifying that you wish to focus on dividend investments when going through the questionnaire, Fineco will take care of the rest. Like all of the stock brokers that we discuss on this platform, Fineco is licensed by the FCA. It is also covered by the FSCS – so your funds are always kept safe.

Pros:

- No commissions or inactivity fees

- Includes portfolio management tools

- Excellent fundamental analysis and commentary

- Simple system for tracking investment performance

Cons:

- 25% annual management fee

Your capital is at risk

3. IG – Trusted UK Broker With ISA Accounts

Last but certainly not least – IG is another UK broker that is worth considering for your dividend investment needs. The platform stands out for the 12,000+ financial assets that it hosts. This covers everything from stocks and ETFs to investment trusts and mutual funds.

All in all, if there is a dividend investment you are interested in, it’s likely that IG offers it. The only downside to using IG is that you will pay slightly more than the other brokers discussed above. This comes in at an entry-level dealing fee of £8.

Only when you place 3 or more orders in the prior month can you get this down to £3. You will, however, be using one of the most trusted brokers in the UK space. Not only has this brokerage firm been active since the early 1970s, but it is now a public-listed company. Take note, minimum deposits start at £250 and you can use a debit/credit card or bank transfer.

Pros:

- Trusted UK broker with a long-standing reputation

- More than 12,000 traditional assets

- Good value share dealing services

- Leverage and short-selling also available

- Spread betting and CFD products

- Various account types

- Great research department

Cons:

- A minimum deposit of £250

- US stocks have a $15 minimum commission

Your capital is at risk

Conclusion

Dividend investments are popular in the UK as they provide a regular, somewhat predictable flow of income. In addition to this, you also stand the chance of increasing the value of your investment through capital gains. This is when your chosen stock, ETF, or fund goes up in price.

All in all, the most important thing is that you diversify to mitigate your long-term risk and consider reinvesting your dividends to ensure your capital grows as quickly as possible.

FAQs

Which UK stocks pay the highest dividends?

Some of the best dividend-paying companies in the UK include Royal Dutch Shell, BP, British American Tobacco, and Legal & General.

How do I collect dividends UK?

First you need to open an account with an online broker and proceed to deposit funds. If and when your assets generate dividends, this will be paid directly into your brokerage account. You can withdraw the cash or invest it into other assets.

Is dividend investing a good strategy?

Dividend investing is a great long-term strategy to consider. With that said, you can further enhance this strategy by reinvesting your dividends as soon as they are received.

Can you live off of dividends?

Being abe to supplement your lifestyle through full-time dividends is the dream of many in the UK. However, in order to achieve this, you would need to a considerable amount of money. And of course - it will also depend on the yield you get from your dividend investments.

Do you need to pay tax on UK dividend investments?

All UK residents can earn up to £2,000 worth of dividends per year without paying any tax. After that, your dividend might be liable for tax. One such way to reduce your tax liability is to open a Stocks and Shares ISA.

What are the best dividend investments in the UK?

If you're a complete newbie that wants to combine dividend investing with a passive form of income, then you might be best to opt for an ETF. In particular, you'll want to choose on ETF that focuses exclusively on dividend investments.

Kane Pepi

Kane Pepi

View all posts by Kane PepiKane Pepi is a British researcher and writer that specializes in finance, financial crime, and blockchain technology. Now based in Malta, Kane writes for a number of platforms in the online domain. In particular, Kane is skilled at explaining complex financial subjects in a user-friendly manner. Academically, Kane holds a Bachelor’s Degree in Finance, a Master’s Degree in Financial Crime, and he is currently engaged in a Doctorate Degree researching the money laundering threats of the blockchain economy. Kane is also behind peer-reviewed publications - which includes an in-depth study into the relationship between money laundering and UK bookmakers. You will also find Kane’s material at websites such as MoneyCheck, the Motley Fool, InsideBitcoins, Blockonomi, Learnbonds, and the Malta Association of Compliance Officers.

WARNING: The content on this site should not be considered investment advice and we are not authorised to provide investment advice. Nothing on this website is an endorsement or recommendation of a particular trading strategy or investment decision. The information on this website is general in nature, so you must consider the information in light of your objectives, financial situation and needs. Investing is speculative. When investing your capital is at risk. This site is not intended for use in jurisdictions in which the trading or investments described are prohibited and should only be used by such persons and in such ways as are legally permitted. Your investment may not qualify for investor protection in your country or state of residence, so please conduct your own due diligence or obtain advice where necessary. This website is free for you to use but we may receive a commission from the companies we feature on this site.

Buyshares.co.uk provides top quality insights through financial educational guides and video tutorials on how to buy shares and invest in stocks. We compare the top providers along with in-depth insights on their product offerings too. We do not advise or recommend any provider but are here to allow our reader to make informed decisions and proceed at their own responsibility. Contracts for Difference (“CFDs”) are leveraged products and carry a significant risk of loss to your capital. Please ensure you fully understand the risks and seek independent advice. By continuing to use this website you agree to our privacy policy.

Trading is risky and you might lose part, or all your capital invested. Information provided is for informational and educational purposes only and does not represent any type of financial advice and/or investment recommendation.

Crypto promotions on this site do not comply with the UK Financial Promotions Regime and is not intended for UK consumers.

BuyShares.co.uk © 2026 All Rights Reserved. UK Company No. 11705811.

We use cookies to ensure that we give you the best experience on our website. If you continue to use this site we will assume that you are happy with it.Scroll Up