Best Stocks and Shares ISA 2023 – Cheap ISAs Compared

If you’re based in the UK and looking to invest in the financial markets, a stocks and shares ISA is a popular topic to research. This is because some ISAs enable investments of up to £20,000 with little to no tax whatsoever on those investments. In this guide, we explore some of the UK’s stocks and shares ISAs in 2023.

On top of discussing the some popular providers currently active in the market, we also review how stocks and shares ISA work.

Key Takeaways on Individual Savings Accounts

- Individual Savings Accounts or ISAs for short, are different from typical savings accounts in that they eliminate tax on investment returns.

- There’s an annual ISA budget that caps the amount of money a trader can put into an ISA. At the moment, this stands at £20,000.

- One of the most attractive features of an individual savings account is that investors can avoid paying tax on dividend stocks.

Popular Stocks and Shares ISA Accounts

Let’s briefly run through a list of the popular stocks and shares ISA accounts and then we’ll dive into detailed reviews of each:

- Fineco Bank

- Hargreaves Lansdown

- Halifax

- Interactive Investor

- AJ Bell

- Barclays

- The Share Centre

- Santander

- Vanguard

- Fidelity

- HSBC

Popular Stocks and Shares ISAs 2023

As noted earlier, investing in a stocks and shares ISA means signing up with a UK stock broker. As such, you need to do some homework to ensure the platform is right for you and your long-term investing goals.

The following providers are considered to be the most popular Stocks and Shares ISAs of 2023.

1. Fineco Bank

Fineco Bank is considered to be the most popular UK stocks and shares ISA. The broker currently has a promotion that offers zero account fees when you open a new ISA, and the account fee is just 0.25% of your total portfolio once the promotion ends. On top of that, investing in ETFs with Fineco Bank is always free and there’s no exit fee if you want to transfer your ISA in the future.

Fineco Bank is considered to be the most popular UK stocks and shares ISA. The broker currently has a promotion that offers zero account fees when you open a new ISA, and the account fee is just 0.25% of your total portfolio once the promotion ends. On top of that, investing in ETFs with Fineco Bank is always free and there’s no exit fee if you want to transfer your ISA in the future.

Fineco Bank gives you access to thousands of individual shares and ETFs, so traders can put together their own custom portfolio. Share dealing costs just £2.95 per deal for UK shares and $3.95 per deal for US shares, making Fineco Bank far cheaper for active investing than any of the other stocks and shares ISAs we’ve reviewed. Fineco Bank allows users to open a new ISA and start investing with as little as £100.

Another feature of Fineco Bank is that investors cans manage their stocks and shares ISA online or through the broker’s mobile app. Fineco also supports buying and selling funds on the go, and the use of the global fund screener to find investment ideas.

Your capital is at risk.

2. Hargreaves Lansdown

Hargreaves Lansdown is a market leader in the UK brokerage scene. On top of a fully-fledged research department and highly extensive offering of equities, the platform offers stocks and shares ISAs. You have two options when it comes to investing with a Hargreaves Lansdown stocks and shares ISA – DIY or ready-made portfolios.

Hargreaves Lansdown is a market leader in the UK brokerage scene. On top of a fully-fledged research department and highly extensive offering of equities, the platform offers stocks and shares ISAs. You have two options when it comes to investing with a Hargreaves Lansdown stocks and shares ISA – DIY or ready-made portfolios.

If opting for the former, you will be selecting from over 2,500 shares, funds, and trusts yourself, meaning you retain full control of where your money goes. Helpfully, the broker offers fund shortlists for popular investment types like Funds for Income, Seeking Retirement Income Funds, and Established Trackers. Hargreaves Lansdown does offer individual stock investing, but the research tools available for this purpose are relatively limited.

Traders can invest in a Hargreaves Lansdown stocks and shares ISA from just £100. Alternatively, the broker lets you get started from £25 per month if you set up recurring investments. If opting for a ready-made portfolio, Hargreaves Lansdown will create a basket of shares on your behalf – based on your investment needs and attitude to risk.

This requires a minimum investment of £1,000. Both options carry an annual charge of 0.45%, and you then need to take share dealing charges into account. This can be as high as £11.95 at Hargeaves, so do bear this in mind.

Your capital is at risk.

3. Halifax

![]() Halifax Bank offers a stocks and shares ISA to customers and non-customers alike. The broker is a subdivision of Lloyds, the investment giant, but it’s operated wholly independently and is much more geared towards long-term investors.

Halifax Bank offers a stocks and shares ISA to customers and non-customers alike. The broker is a subdivision of Lloyds, the investment giant, but it’s operated wholly independently and is much more geared towards long-term investors.

Halifax is considered suitable for those that don’t want to be inundated with too much choice. That is to say, Halifax offers a relatively small selection of investment options, as well as three ready-made portfolios. In total, the broker has around 2,000 mutual funds, 575 exchange-traded funds (ETFs), and nearly 300 investment trusts.

In terms of fees, there is a 0.24% platform charge and a 0.25% charge if using the fund management services. When it comes to share dealing charges, this stands at £12.50 per trade. There’s also an additional charge for buying shares listed outside the UK. This can make it somewhat expensive.

There are no early account closure fees at Halifax, so investors can take their money out whenever they see fit.

Your capital is at risk.

4. Interactive Investor

Interactive Investor is an online stock broker that offers one of the most popular stocks and shares ISA plans. This broker, you get access to over 40,000 investment options. This includes a full library of UK and international stocks, as well as ETFs and funds. Some users could also invest in US stocks with the Interactive Investor stocks and shares ISA, which is a plus for more aggressive investors.

Interactive Investor is an online stock broker that offers one of the most popular stocks and shares ISA plans. This broker, you get access to over 40,000 investment options. This includes a full library of UK and international stocks, as well as ETFs and funds. Some users could also invest in US stocks with the Interactive Investor stocks and shares ISA, which is a plus for more aggressive investors.

In terms of pricing, Interactive Investor might be suitable for you if you are looking to invest on a monthly basis. That is to say, you plan to trade once per month. This is because the broker charges a hefty monthly fee of £9,99, but, this allows one free trade per month. As such, you aim to purchase shares in one company per month, you are effectively paying £9.99 per order. While that’s not cheap, it’s very competitive compared to brokers like Halifax.

The platform has been in business for over three decades, and it also offers market insights to help you in the decision-making process. Investors also take advantage of automatic dividend reinvestments and recurring monthly investments.

Your capital is at risk.

5. AJ Bell

AJ Bell offers a Junior Stocks and Shares ISA accounts in addition to standard ISAs. It can be opened in just a few minutes and invest up to £9,000 per year tax-free.

AJ Bell offers a Junior Stocks and Shares ISA accounts in addition to standard ISAs. It can be opened in just a few minutes and invest up to £9,000 per year tax-free.

In addition, while some UK investors like to inject a one-off lump sum, others prefer to pay a bit at the end of each month. If the latter sounds like you, then it might be worth considering AJ Bell. This is because the share dealing platform offers one of the most popular stocks and shares ISA accounts and allows you to pay just £1.50 when you set up a monthly direct debit.

This broker allows users to do this from just £25 per month. In terms of investment options, you’ll have access to a wide range of stocks and shares, and over 2,000 ETFs, investment trusts, and funds.

If you have more than £4,000 in your AJ Bell stocks and shares ISA, you will get free access to the platform’s Shares magazine. You will have full control over your investments, which you execute online or via the broker’s mobile app.

Your capital is at risk.

6. Barclays

![]() Much like Halifax, Barclays is a UK bank that offers one of the leading stocks and shares ISA accounts. Its platform is basic to use, so you don’t need to have any prior experience of buying and selling shares online. Although the fee structure at Barclays is somewhat confusing at first glance, it does work out fairly competitive – especially in terms of annual fees.

Much like Halifax, Barclays is a UK bank that offers one of the leading stocks and shares ISA accounts. Its platform is basic to use, so you don’t need to have any prior experience of buying and selling shares online. Although the fee structure at Barclays is somewhat confusing at first glance, it does work out fairly competitive – especially in terms of annual fees.

So, funds work out at just 0.2% per year, which is much cheaper than the 0.45% charged by Hargreaves Lansdown. Flat customer fees amount to a minimum of £4. But, all customer fees (including the annual fund charge) is capped at £125 month. That’s pretty fair in our opinion.

When it comes share dealing charges, standard stocks and shares cost £6 per trade, while funds are cheaper at £3 per trade. If you place your orders over the phone, an additional transaction fee of £25 will apply. Much like AJ Bell, Barclays will credit any transfer fees that are charged by your prior provider up to the first £500.

Barclays has over 2,000 funds to choose from, plus stocks from more than 35 exchanges around the world. Beginner investors can also take advantage of 5 ready-made funds designed for any investing goal.

Your capital is at risk.

7. Wealthify

![]()

Wealthify is an automated investment platform, also known as a robo advisor, launched in 2016. The platform helps UK residents effortlessly invest for retirement by offering several types of risk-balanced, long-term portfolios. As your investments grow, Wealthify keeps your portfolio in balance and makes adjustments as needed over time.

Wealthify was acquired by Aviva in 2017 and now operates as a subsidiary of the UK insurance giant. However, Wealthify continues to operate independently and is run by its original leadership team. Wealthify does not publicize its total assets under management, but the platform has over 30,000 users in the UK.

Wealthify offers a Stocks and Shares ISA account, which is free from capital gains tax. However, traders are only permitted to deposit up to £20,000 per year in an ISA.

Your capital is at risk.

8. Santander Stocks and Shares ISA

The Santander stocks and shares ISA is a flexible account that offers several different ways to invest. If you want to make investing as simple as possible, Santander offers 4 pre-made investment funds for you to choose from. On the other end of the spectrum, Santander has a self-directed investment hub offering thousands of stocks, ETFs, mutual funds, and more. You’ll find shares not only from the UK, but also from all of the major US, European, and Asian stock exchanges.

The Santander stocks and shares ISA is a flexible account that offers several different ways to invest. If you want to make investing as simple as possible, Santander offers 4 pre-made investment funds for you to choose from. On the other end of the spectrum, Santander has a self-directed investment hub offering thousands of stocks, ETFs, mutual funds, and more. You’ll find shares not only from the UK, but also from all of the major US, European, and Asian stock exchanges.

In between, Santander has tier of assisted investing. This service isn’t free with your account, but it can be much cheaper than paying for an outside financial advisor. In fact, if you want help putting together your investment portfolio, Santander’s stocks and shares ISA is one of the most cost-effective options around.

Santander allows you to start investing with a minimum deposit of £5,000 or a monthly recurring investment of £20. If you want to take advantage of face-to-face financial advice, you must have at least £20,000 in your ISA. The provider charges a 0.35% annual fee on the first £50,000 in your ISA.

Your capital is at risk.

9. Vanguard

The provider is one the largest and most prevalent in the global fund scene. Users have access to over 75 funds, all of which are personally managed by the team at Vanguard. This particular stocks and shares ISA is also one of the most cost-effective.

The provider is one the largest and most prevalent in the global fund scene. Users have access to over 75 funds, all of which are personally managed by the team at Vanguard. This particular stocks and shares ISA is also one of the most cost-effective.

This is because you will pay just 0.15% per year in account fees. Any buy and sell trades that Vanguard performs on your behalf will not subject to a flat trading fee like you would have to pay elsewhere. In terms of account minimums, some traders could invest a lump sum of £500 or more, or commit to a monthly direct debit of £100.

Overall, these terms make Vanguard one of the cheapest platforms for long-term investing. However, note that the selection of individual shares is limited.

Your capital is at risk.

10. Fidelity

Much like in the case of Vanguard, Fidelity is a global leader in the ETF and fund space. With that said, the platform has since opened its doors to the stocks and shares ISA arena. By opening an account, you will have access to heaps of funds from a variety of markets.

Much like in the case of Vanguard, Fidelity is a global leader in the ETF and fund space. With that said, the platform has since opened its doors to the stocks and shares ISA arena. By opening an account, you will have access to heaps of funds from a variety of markets.

One thing that’s worth noting about Fidelity is that the brokerage is taking over ISAs from Legal and General, one of the UK’s biggest investment firms. Legal and General is not accepting new ISA accounts at this time, and all current accountholders are being moved to Fidelity.

Once again, you will be going directly with the provider when investing in funds. Fees are somewhat reasonable, although they could be cheaper. This is because you will pay 0.35% per year – but only if you invest £7,500.

Your capital is at risk.

11. HSBC Stocks and Shares ISA

This bank and brokerage firm allows you to open a stocks and shares ISA with just £50 if you want investment advice and just £100 if you want to direct your own investment strategy. The firm charges a 0.5% fee for investment advice, which also makes it a fairly affordable option for new investors to get into the market.

This bank and brokerage firm allows you to open a stocks and shares ISA with just £50 if you want investment advice and just £100 if you want to direct your own investment strategy. The firm charges a 0.5% fee for investment advice, which also makes it a fairly affordable option for new investors to get into the market.

HSBC has a somewhat limited selection of funds to choose from if you plan to use the company’s advice. There are 450 investment funds available in the HSBC Global investment Centre.

If you’re choosing your own investments, you have access to thousands of shares and ETFs from the UK, US, and around the world. HSBC charges a dealing fee of £10.50 per trade for UK shares and a quarterly account fee of £10.50. These charges aren’t cheap, particularly if you’re buying shares in small increments.

Your capital is at risk.

What is a Stocks and Shares ISA?

In its most basic form, an Individual Savings Account, or simply ISA, is a government initiative that aims to promote investments. That is to say, you will have the chance to shield some of your investment-related tax obligations – up to a certain amount each year.

In its most basic form, an Individual Savings Account, or simply ISA, is a government initiative that aims to promote investments. That is to say, you will have the chance to shield some of your investment-related tax obligations – up to a certain amount each year.

While there are several ISAs to choose from, a stocks and shares ISA is what you will want to look at if you plan to invest in the stock markets. In the 2020/21 tax year (6th April 2020 to 5th April 2020), your stocks and shares ISA comes with a limit of £20,000.

In other words, the first £20,000 that you invest in the stock markets will not be liable for tax. Ordinarily, gains that you make from a share investment would be liable for capital gains tax and dividends tax. Regarding the former, this is the amount of money that you make when you sell your shares. For example, if you buy £2,000 worth of BP shares and sell them for £3,000 – your capital gains are £1,000.

Without the aid of an ISA, you might be required to pay tax on this £1,000, depending on your individual circumstances. When it comes to dividends, anything you make after the first £2,000 would also be liable for tax. Once again, making use of a stocks and shares ISA means that users can shield these tax obligations, up to the first £20,000.

How do Stocks and Shares ISAs Work?

Before we run you through a numerical example of how a stocks and shares ISA works, it is important to explain the fundamentals. That is to say, stocks and shares ISAs are simply dedicated brokerage accounts. For example, let’s suppose that you open an account with Hargreaves Lansdown.

In doing, you would have access to both an ordinary brokerage account and a stocks and shares ISA account. Although this means that you will be choosing shares on a DIY basis, the first £20,000 will go through the ISA. Anything after that will be liable for capital gains and dividends tax in the standard way.

Ultimately – and as we discuss in more detail later on, the ISA you go with will be based on underlying broker. For example, you’ll need to explore metrics such as share dealing fees, the types of stocks to invest in, customer support, and whether the platform is regulated and protected by the FCA/FSCS.

Nevertheless, here is a example of how a stocks and shares ISA works.

Example of Stocks and Shares ISA

- You open a stocks and shares ISA with your chosen broker

- You invest £5,000 into Tesco, HSBC, Royal Mail, and Netflix.

- This means that you have invested a total of £20,000 – which equals your full stocks and shares ISA allowance for the year

- At the end of year one, your £20,000 portfolio is now worth £25,000

- You have also received £3,000 in dividend payments

- If you were to sell your holdings, your overall investment is now worth £28,000 (£25,000 share value + £3,000 dividends)

- As this £28,000 is based on your original £20,000 ISA allowance, you would not need to pay any capital gains or dividends tax on your earnings

Ordinarily, the £8,000 gains that you made (£5,000 + £3,000) likely would have been liable for tax. But, by utilizing your full ISA allowance, you were able to shield these profits.

Read our comprehensive guide on tax on shares here.

Benefits of Stocks and Shares ISAs

- Tax-Efficient: It can be frustrating to see your investments grow, only to then lose a chunk of your profits through capital gains and dividends tax. As we have already noted, the main benefit of a stocks and shares ISA is that you will get to shield the first £20,000 from HMRC. By investing in shares outside of an ISA, you will all-but-certainly need to pay something to the taxman.

- Annual Allowance Refreshes Each Year: It is important to note that you will get a new stocks and shares ISA allowance every year. So, if you reach your £20,000 limit in the 2020/21 tax year, you can invest an additional £20,000 the following year. The figures for 2022/23 are yet to be announced by the government, so it is hoped that an increased allowance comes into play.

- Heaps of Brokers to Choose From: With stocks and shares ISAs being a no-brainer for UK investors, more and more stock brokers are offering dedicated ISAs. As such, finding the highest performing stocks and shares ISA that meets your needs should no longer be an issue.

- Compound Interest, Tax-Free: Let’s suppose that you invest £20,000 into your ISA in 2023, and then leave the respective stocks and shares untouched for the next 20 years. Based on a theoretical annualized average return of 7.75% on the FTSE 100, your money would be worth just under £90,000 – and that’s without taking dividends into account. As such, when you eventually came around to selling the shares, you would be able to do so without paying a single penny in capital gains tax!

- Safe and Regulated: Online brokers offering stocks and shares ISAs to UK investors must be in receipt of an FCA license. In the vast majority of cases (check this before taking the plunge), this also means that your funds will be protected by the FSCS. This means that were the broker to go bust, the first £85,000 would be safeguarded.

How Much Does a Stocks and Shares ISA Cost?

One of the potential downsides to investing through a popular stocks and shares ISA is that they come with fees. Most stocks and shares ISAs charge a commission on every trade you make as well as an annual account fee. In addition, there may be a fee if you don’t place any trades for a length of time (an inactivity fee).

Let’s see how the stocks and shares ISAs match up against each other in terms of fees.

| Brokers | Charge per Trade (shares) | Annual account fee | Inactivity Fee |

| Fineco Bank | £2.95 (UK shares) | Free until April 2022, then 0.25% on first £250,000 | None |

| Hargreaves Lansdown | £5.95 – £11.95 depending on number of trades in previous month | 0.45% on first £250,000 | None |

| Halifax | £12.50 | £12.50 | £10 after 12 months |

| Interactive Investor | £7.99 | £199.88 | £10 after 24 months |

| AJ Bell | £4.95 – £9.95 depending on number of trades in previous month | £0.25% | £10 after 24 months |

| Barclays | £6 | £0.1% | £10 after 24 months |

| Wealthify | £7.50 (or 1% for trades above £750) | £60 | £10 after 24 months |

| Santander | £2.95 | £0.35% | £10 after 24 months |

| Vangaurd | £0 | 0.15% | £10 after 24 months |

| Fidelity | £10 | £45 or 0.35% | £10 after 24 months |

| HSBC | £10.50 | £42 | None |

What Type of Investments Can You Invest in with a Stocks and Shares ISA?

As the name suggests, a stocks and shares ISA enables you to invest in stocks and shares. But that doesn’t mean you’re only limited to picking individual stocks.

- Stocks or shares: Shares are slices of ownership in an individual company. Buying individual shares can be riskier than buying funds.

- ETFs: Exchange-traded funds are baskets of stocks. They may seek to track the performance of a market index like the FTSE 100, or they could invest in companies that fit into a specific market sector or theme. Typically, ETFs have low ongoing management fees.

- Investment funds: Also known as mutual funds, these are collective investments in which you pool your money with other investors. A fund manager then invests that money on all the investors’ behalf. Investment funds can invest in not only stocks, but also real estate, bonds, art, or riskier investments. They typically charge higher fees than ETFs.

- Investment trusts: Investment trusts are publicly-listed companies that closely resemble ETFs. Like ETFs, they are controlled by a fund manager who invests the money in the trust.

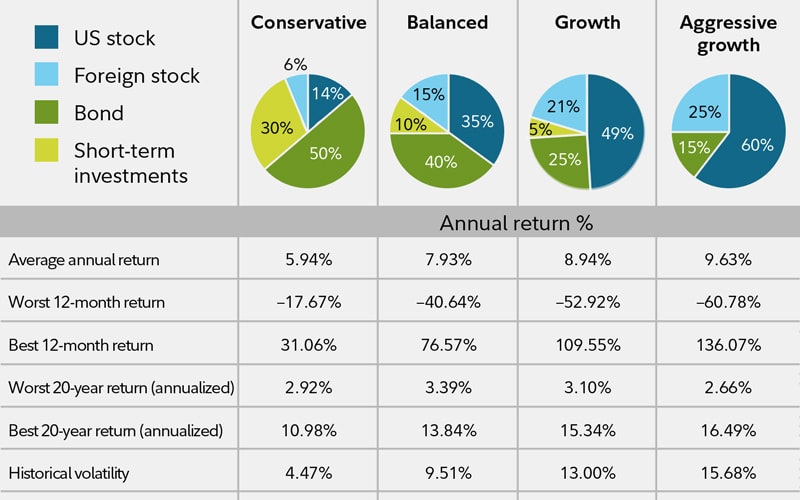

Stocks and Shares ISA Returns – How Much Can I Expect to Make?

One of the most common questions investors ask is how much they can expect to make when investing in a stocks and shares ISA. The thing about investing is that it’s difficult to say for sure. If the stock market shoots up and you’re invested in the right place at the right time, you could double your money. Of course, there’s also a chance that the stock market crashes. If that happens, you could lose money.

So, most investors can expect to make between 7-12% per year simply by investing in a fund that tracks the UK or US stock markets. If you are investing in ETFs, mutual funds, or investment trusts, look at how the fund has performed since inception and especially during periods when the stock market dropped.

Comparison Table of Stocks and Shares ISA in UK

| Brand | Minimum Initial Deposit | Minimum Monthly Investment | Minimum Lump Sum Stocks & Shares ISA Investment | Invest in | Permanent UK Resident |

| Hargreaves Lansdown | £100 | £25 | £100 | Over 3,000 funds | Yes |

| Fineco Bank | £100 | £0 | £100 | Over 2,000 funds | Yes |

| Halifax | £0 | £0 | £100 | Over 2,000 funds | Yes |

| Interactive Investor | £0 | £9.99 | £200 | Over 1,500 funds | No |

| AJ Bell | £1.50 | £25 | £250 | Over 2,000 funds | Yes |

| Barclays | £200 | £4 | £100 | Over 2,000 funds | Yes |

| Wealthify | £1 | £5 | £150 | Over 1,500 funds | Yes |

| Santander | £5,000 | £20 | £200 | Over 3,000 funds | Yes |

| Vanguard | £100 | £100 | £500 | Over 1,500 funds | Yes |

| Fidelity | £25 | £0 | £100 | Over 2,000 funds | Yes |

| HSBC | £50 | £0 | £200 | Over 2,000 funds | Yes |

How to Choose Stocks and Shares ISAs

So now that you have had some time to review some of the UK’s stocks and shares ISAs, we now need to discuss some of the key metrics that you need to look out for prior to taking the plunge. After all, you need to ensure that your chosen platform is right for your individual needs – as no-two brokers are the same.

This should include:

Tradable Assets

Firstly, you need to check what assets the stocks and shares ISA will allow you to invest in. For example, while some platforms only support UK shares, others give you access to the shares to buy from markets in the US, Europe, and more.

In other cases, you might have access to a plethora of ETFs, funds, and investment trusts. All in all, you need to ensure that the stocks and shares ISA allows you to invest in your preferred asset class.

Annual Fees

Most UK stocks and shares ISAs will charge you an annual fee. As frustrating as this can be, you need to remember that you have the potential to save thousands of pounds in capital gains and dividends tax.

The annual fee is typically expressed as a percentage, which is then multiplied by the amount you have invested. For example, if the platform charges 0.3%, and you utilized your full allowance, this would translate into an annual cost of just £60

Trading Fees

Every time you buy or sell shares through your stocks and shares ISA, you will need to pay a trading fee, so you’ll want to find the most popular stocks and shares ISAs for you with the lowest fees. Otherwise referred to as a share dealing charge, this is often a flat fee.

Transfer Fees

Be very careful to assess where the broker stands with transfer fees. This is a fee charged when you decide to transfer your stocks and shares ISA to another provider. Not all brokers charge one, but you need to check nonetheless.

At the other end of the spectrum, some brokers will cover the transfer fee when you import your stocks and shares ISA from another provider.

Research and Educational Tools

If you’re planning to invest on a DIY basis, then you will need all of the help that you can get. At the forefront of this a stocks and shares ISA provider that offers heaps of research and educational tools, especially if you’re a beginner want to learn how to invest in stocks.

Regarding the latter, this should include some handy guides on how ISAs work, and what you need to do to build a healthy portfolio. In the research department, this should include fundamental news and market insights.

When Can You Invest in a Stocks and Shares ISA?

In a nutshell, users can invest in the most popular stocks and shares ISA UK whenever they see fit. The most important thing to remember is that ISAs operate on a year-to-year basis. That is to say, the 2020/21 year operates from April 6th 2020 to April 5th 2021.

In a nutshell, users can invest in the most popular stocks and shares ISA UK whenever they see fit. The most important thing to remember is that ISAs operate on a year-to-year basis. That is to say, the 2020/21 year operates from April 6th 2020 to April 5th 2021.

In other words, traders can invest the entire £20,000 in one go, or instead inject small amounts throughout the year.

This simply means that you won’t benefit from any tax-savings on the surplus investments. Then, when the next tax year comes into play, you can start working towards your newly reset allowance.

What Are the Risks of Stocks and Shares ISAs?

The risks of investing in a stocks and shares ISA are much the same as any other investment opportunity. Put simply, there is every chance that you could lose money. After all, when you buy shares, there is no guarantee that the value of the stocks will go up. On the contrary, the shares could decrease in value. If this is the case – it is irrelevant whether you have the shares in an ISA, as you will not have any capital gains to shield from HMRC!

The fact of the matter is this – if you do not want to take on any risks whatsoever, then a stocks and shares ISA will not be for you. Instead, you will likely be suited for savings bonds that are backed by the FSCS. Sure, you won’t stand to lose any money (up to the first £85,000), you will be lucky to earn more than 1-2% per year. Ultimately, the investment arena is all about risks and returns, so do bear this in mind.

Are Stocks and Shares ISAs Covered by the Financial Services Compensation Scheme?

The Financial Services Compensation Scheme (FSCS) protects up to £85,000 of money and investments inside investing accounts in the event that your broker runs into financial trouble or goes out of business. This won’t stop you from suffering losses when the market drops, but it does eliminate some of the risk that comes with giving your money to a broker.

How to Build a High Performing Stocks and Shares ISA

The most challenging part of the process is knowing how to pick stocks and shares for the ISA. With that in mind, below you will find some tips on building a high performing stocks and shares ISA.

Tip 1. Ensure Your Portfolio is Diversified

Without a doubt, the most important tip that we can bring to you is with respect to diversification. Put simply, diversification means that you will not be putting all of your eggs into one basket. An example of this would be investing your full £20,000 ISA allowance into a single company like Facebook.

Instead, a well-diversified portfolio would see your £20,000 allocated into dozens, if not hundreds of different shares. In fact, by investing £100 into each stock, you would have a portfolio of 200 companies! Take note, if you don’t go the ETF or index route, make sure that you know how much you are paying for each individual trade.

For example, if you use a stocks and shares ISA that charges £7.50 per trade, a portfolio of 200 stocks would cost you £1,500 in fees! If you were to pay a variable fee of, say 1%, this would cost just £200 when investing the full £20,000.

Tip 2. Create a Risk-Based Portfolio

A risk-based portfolio will consist of investments from a variety of risk levels. To keep things simple, this would be investments that are considered low, medium, and high risk. Sure, some of you might be looking to build the entire portfolio with low-risk assets, but in order to grow your money faster, it is also worth considering adding a small percentage of medium and high-risk assets. Of course, the amount of risk that you take is entirely down to what you feel comfortable with.

Nevertheless, a well-balanced portfolio might consist of:

- 70% in high-grade stocks: This would consist of stable, strong, and highly established stocks like Amazon, Apple, GlaxoSmithKline, and IBM.

- 20% in medium-grade stocks: These stocks will still form part of a major index like the FTSE 100 or NASDAQ, but they come with slightly higher levels of risk. An example of this is Uber – a multi-billion pound company that is yet to make a profit. While the firm has a global presence and could potentially be worth significantly more in the future, its ever-growing debt levels do come with added risks.

- 10% in low-grade stocks: These are essentially high-risk, high-return stocks. They could, for example, be firms listed on the Alternative Investment Market (AIM), or a company that is currently experiencing financial difficulties. Either way, you should probably avoid adding more than 10% of your stock portfolio from this category.

Tip 3: Forget DIY Investing, Opt for a Fund

While you might enjoy the thrill of picking shares on a DIY basis, the overarching objective should be to grow your money over time. As a newbie investor, this can be a challenging task when you are required to pick shares yourself. As a result, why not consider a fund of some sort so that you can leave the decision-making process to the expects?

In a nutshell, ETFs, mutual funds, and investment trusts allow you to invest in a passive manner. Once you invest money into the fund, the fund manager will take care of the rest. Crucially, this means that the fund provider will be buying and selling investments on your behalf.

Comprehensive List of UK Stocks and Shares ISAs

We’ve already had a look at some stocks and shares ISAs, but there are many more out there. Here’s a comprehensive list of UK stocks and shares ISAs:

- Fineco Bank

- Hargreaves Lansdown

- Halifax

- Interactive Investor

- AJ Bell

- Barclays

- The Share Centre

- iWeb

- Vanguard

- Fidelity

- Cavendish

- Santander

- Legal and General

- Standard Life

- Aegeon

- Equiniti

- Selftrade

- Scottish Mortgage

Conclusion

While the viability of a cash ISA is debatable if you’re from the UK and you plan to invest in the financial markets, investing with the stocks and shares ISA UK is a no-brainer. After all, you will be able to invest up to £20,000 in the current (and next) tax year, without having any of your capital gains or dividends liable for tax.

With that said, you still need to do lots of homework before taking the plunge. Not only should this include research on your chosen investments, but also on the respective stocks and shares ISA provider, too. Crucially, just because you are shielding your capital gains from tax, this isn’t to say that you are guaranteed to make money.

Frequently Asked Questions about ISAs

How does a stocks and shares ISA work?

How much can I put in a stocks and shares ISA?

What is a stocks and shares ISA?